GST Returns 2.0 – New return filing mechanism

The GST Council in its 27th meeting, held on 4 May 2018, had approved the basic principles of GST return design. Later in the 28th meeting, held on 21 July 2018, the GST council approved the key features and the broad format of the GST returns. The proposed returns have now been made available on the GSTN portal for feedback and recommendations.

The core objectives of the new return filing system are as follows:

- Linking the recipient’s Input Tax Credit (ITC) with the supplies declared by the supplier

- Simpler compliances for small taxpayers

- Consolidating GSTR-1 and GSTR-3B into a single return

- Making GST returns user-friendly

Earlier, the new GST return filing system was expected to be made available on a voluntary basis from April 2019, and mandatory from July 2019. However, the government has not announced any timeline while releasing the draft formats.

Types of returns

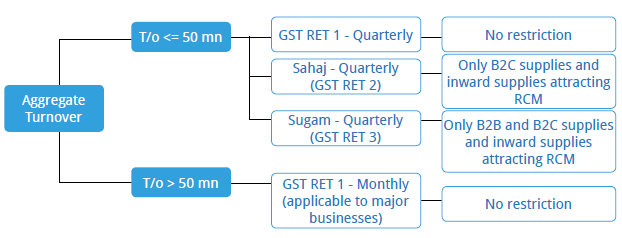

The periodicity of the return filing is based on the aggregate turnover of the preceding financial year. However, the type of return to be filed quarterly by the taxpayers is based on the types of supplies they can disclose in the returns. The same has been explained in the below illustration:

Key points to note

- Filing of quarterly returns is an option available with the small taxpayers, i.e., they can choose to file GST RET-1 on a monthly basis

- Taxpayers filing ‘Sahaj’ and ‘Sugam’ returns can make nilrated, exempt or non-GST supplies

- Taxpayers filing ‘Sahaj’ and ‘Sugam’ returns are not allowed to claim ITC in respect of missing invoices, i.e., invoices not uploaded by the supplier.

FORM GST ANX-1

Annexure of outward supplies, imports and inward supplies attracting reverse charge [to be updated continuously]

What will it cover?

Details of all outward and inward supplies attracting reverse charge and import of goods and services are required to be disclosed in this form. This is similar to GSTR-1.

When to file?

The supplier can upload details in the documents of outward supplies on a real-time basis.

How is the supplier’s liability calculated?

The documents of outward supplies uploaded by the supplier are accounted for towards the tax liability of the supplier.

What are the implications if a document is rejected by the recipient?

A rejected document may be edited before filing any subsequent return by the supplier. ITC in respect of the document so edited or uploaded shall be made available through the next GST ANX-2 to the recipient. However, the liability for such edited documents will be accounted for in the tax period in which the documents have been uploaded by the supplier.

Till when can the details be edited? Editing/amending the details of an uploaded invoice is allowed till the 10th of the following month.

How the recipients ITC is linked? Recipients will get Input Tax Credit (ITC) in a particular month/quarter on the basis of the documents uploaded by the supplier up till the 10th of the month in which the return is being filed.

FORM GST ANX-2

Annexure of inward supplies [auto-populated continuously based on details updated by suppliers in GST ANX-1]

What does it contain?

Details of documents uploaded by the suppliers will be auto-populated on a near real-time basis, and can be accepted or reset/unlocked by the recipient.

What action has to be taken by the recipient?

The recipient should ‘accept,’ ‘reject’ or ‘keep pending’ the documents uploaded by the supplier. This facility would be available to the recipient on a continuous basis. GST ANX-2 will be considered as filed, upon filing of the main return, i.e., GST RET-1.

What is the impact of acceptance?

The invoices accepted by the recipient would determine his ITC. Furthermore, a document once accepted by the recipient would not be available for amendment to the supplier. However, a separate facility for the same would be provided.

Which invoices should be rejected?

Any invoice with an error that cannot be corrected through a financial debit/credit note shall be rejected by the recipient. Example:

- The recipient does not agree with some of the details, such as HSN, tax rate, etc.

- GSTIN of the recipient is erroneous, and therefore it is visible in the GST ANX-2 of a registered person who is not concerned with the supply.

What is deemed acceptance?

Any document, which has not been either accepted, rejected or kept pending by the recipient shall be deemed to have been accepted when the recipient files its return.

FORM GST RET-1

Monthly/Quarterly (Normal) return [most fields are auto-populated from GST ANX-1 and GST ANX-2]

What is GST RET-1?

GST RET-1 is essentially a consolidation of GST ANX-1 and GST ANX-2. Most of the items will be autopopulated from GST ANX-1 and GST ANX-2.

Is there a one-step NIL return process?

The facility to file nil return through SMS will be made available if no supplies have been made or received.

Can a recipient claim ITC of invoices that are not uploaded by the supplier?

Provisional ITC in relation to documents not uploaded by the suppliers can be disclosed and availed through GST RET-1.

The illustrative process under the new return filing system

Our illustration is based on invoices issued by a supplier in July 2019, wherein both the supplier and the recipient are filing GST RET-1 on a monthly basis.

1 July to 10 August 2019

- Invoice details to be uploaded by the supplier by this date

- The uploaded invoice details can be edited by the supplier

- The ITC would be available to recipients in the return of July 2019

- Recipient can accept or reset/unlock the invoice

After 10 August 2019

- Recipient can 'accept', 'reject' or 'keep pending' the invoice details uploaded by the supplier in July 2019

- However, if the invoice is accepted after 10 August 2019, the corresponding ITC would be available in the return for the month of August 2019

18 to 20 August 2019

- The facility to upload invoice details will not be available

20 August 2019

- Due date to file GST RET-1 and pay selfassessed taxes

- If invoice is neither rejected nor kept pending by the recipient, then it would be deemed to have been accepted on filing GST RET-1

Amendment to GST Returns

- The new return filing system provides for amendment of GST ANX-1 through GST ANX-1A and GST RET-1 through GST RET-1A.

- The amendments to GST ANX-1 can be filed before the due date for furnishing of return for the month of September following the end of the financial year or the actual date of furnishing a relevant annual return, whichever is earlier.

- The amendment will be based on the tax period and for invoices/ documents reported therein earlier. E.g. If missing details of a document pertaining to July 2019 have been reported in the return of August 2019, then the amendment of such documents shall be made by amending return of July 2019.