|

|||||||||||||

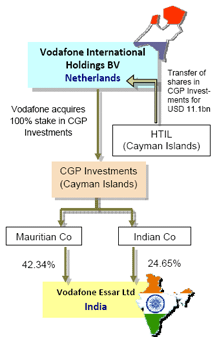

| Tax Implications for Foreign Companies structuring business forays in India | |||||||||||||

| The Vodafone Case Study | |||||||||||||

|

|||||||||||||

|

Writ petition against the SCN is not maintainable

In addition to the above observations, the High Court has also commented about the non‐coperative attitude of Vodafone as under:

Our Comments While the High Court agreed with most contentions of the Revenue, it must be noted that it has not held that Vodafone is liable to pay tax or penalties under the Act in respect of the subject transaction. However, its observations could be a cause for concern from the point of view of cross‐border mergers and acquisitions that involve underlying Indian assets. Foreign investors therefore need to consider the tax implications while structuring business forays in India. A development that would be worth tracking in the future is whether the tax authorities would use this judgment as a basis for dismantling holding company structures that are put through by non residents for investing into India which are covered by certain tax treaty benefits. However, based on international experience, any structure which is backed by 'substance' and confirms to the 'Limitations of Benefits' clauses (both implied and explicit) should pass through these tests. |

|||||||||||||

|